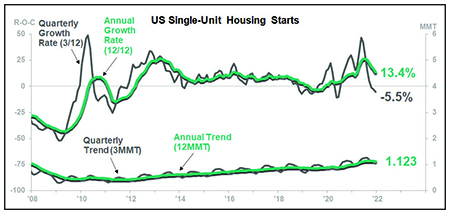

The U.S. industrial sector is on the cusp of transitioning to a slowing growth trend. Our analysis, which includes examining several leading indicators, provides strong evidence that growth rates will be lower in 2022 than in 2021.

U.S. Economy

Despite this slowdown, we do not expect contraction during this cycle. U.S. Industrial Production will rise through the next year, just at a less robust rate than in 2021.

As such, we are entering a dangerous part of the business cycle. This cycle is the crucial period during which firms will likely feel the energy of overall growth but may miss the signs of waning momentum.

Those who ignore the signals emanating from leading indicators may fall into the trap of straight-line budgeting or over-expanding capacity. These signals include the ITR Leading Indicator™ – our proprietary indicator that leads U.S. Industrial Production through the business cycle by about three quarters – and the U.S. ISM Purchasing Managers Index. Be sure to track your business’ performance against the macro economy.

If necessary, adjust your expenditure plans.

Inflation is a top-of-mind economic trend for 2022, especially in construction. The Federal Reserve is beginning to pull back its monetary stimulus, and leading indicators simultaneously move lower. This suggests inflation will be more modest than in 2021.

Inflation rates will cool in 2022 and into late 2023 due to multiple factors, including easing demand during the upcoming macroeconomic slowing growth trend. Lingering supply chain issues will keep inflation elevated in the near term, particularly in the first half of 2022.

In addition to dealing with inflation, consumers are also contending with a less robust U.S. Personal Disposable Income (DPI) trend. We expect DPI to normalize along the lines of the pre-COVID trajectory in the next several months. So, we expect the consumer position to be less strong in 2022 than in 2021. A weakened consumer position will likely result in more price consciousness this year, contributing to the anticipated slowing growth trend in U.S. Total Retail Sales.

We expect Retail Sales to generally rise into 2023, in real and nominal dollars, despite business cycle decline. However, firms should keep a close eye on inventory turns during the backside of the business cycle, as inflation can easily mask real growth issues if you are not closely watching unit levels.

Click Below for the Next Page

![High Performance Contracting: Summit 2018 Panel Discussion on Implementation [PART 1]](https://hvactoday.com/wp-content/uploads/2018/06/DSC_0613-Panel-Discussion-4c3-440x264.jpg)

Recent Comments